01

Real claim language

Every article uses the actual terminology insurers and adjusters use — so when you talk to your insurance company, you sound like someone who knows the rules of the game.

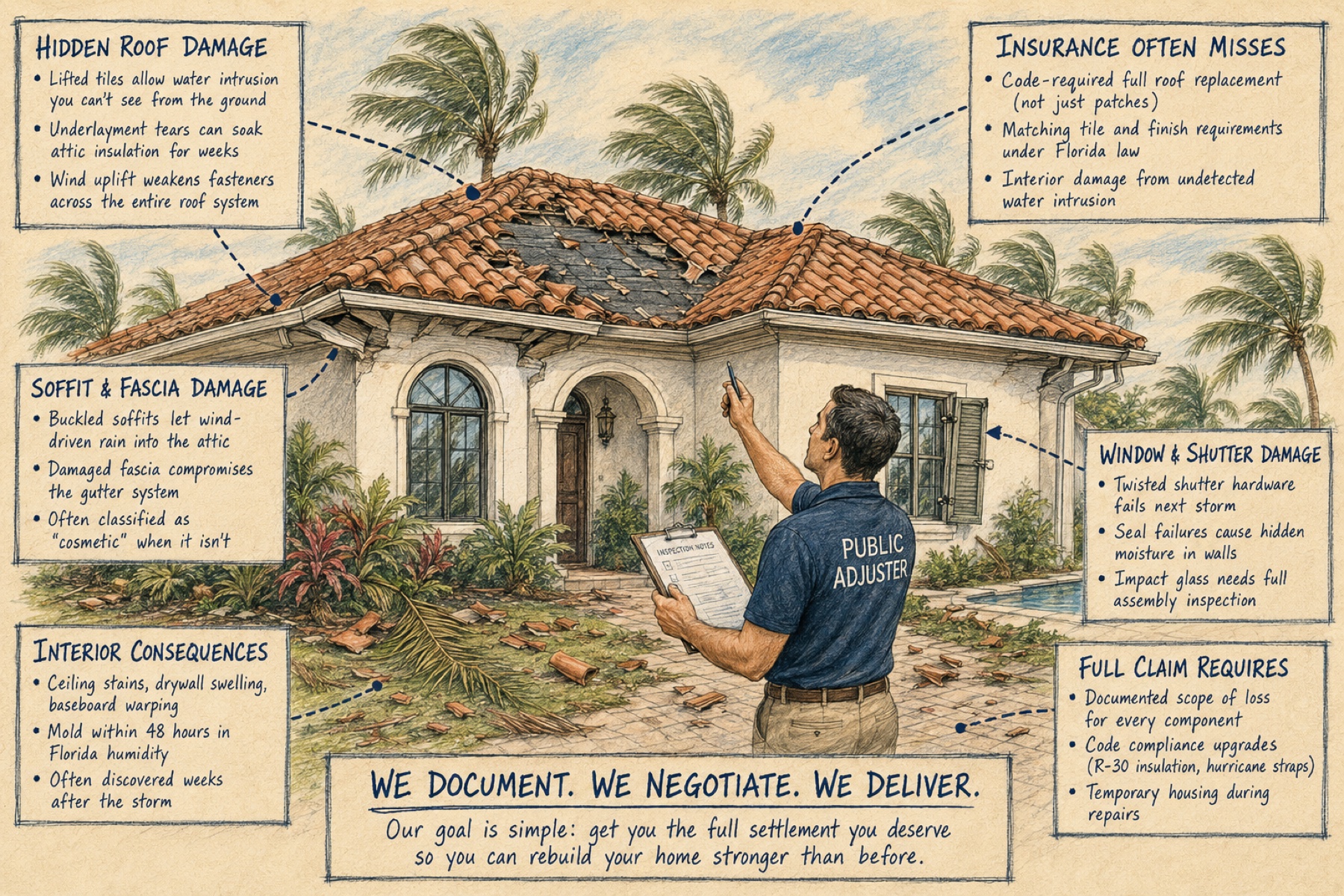

Insurance companies bank on policyholders not understanding their own coverage. Every article here is written by licensed public adjusters who fight these claims for a living — denial tactics, hidden coverage, appraisal strategy, and the documentation that wins settlements.

Free Claim Review

No obligation. We respond within 1 hour during business hours.

Most insurance "advice" online is written by content shops that have never set foot inside a claim file. Generic disclaimers, surface-level tips, and SEO filler dressed up as guidance.

These articles are different. Every piece is written by the team that negotiates these settlements daily — denial tactics we've defeated, appraisal strategies we've used, and the documentation that turns lowball offers into real awards.

Every article uses the actual terminology insurers and adjusters use — so when you talk to your insurance company, you sound like someone who knows the rules of the game.

Not theoretical advice. The exact moves we've used on real files to reverse denials, force fair settlements, and invoke the appraisal clause when negotiation fails.

These resources are free because educated policyholders win bigger claims. Use them whether you hire a public adjuster or fight the claim yourself — the information is yours.

Miami condo HOA insurance claims require expert help. Greenlight Claims helps associations recover full payouts for water, fire, and storm damage — documenting common-area losses, building envelope failures, and shared-system damage that insurers routinely underpay.

Read Article →Miami community associations face complex insurance challenges. We help HOAs document damage and maximize settlements for property losses across shared structures, common areas, and member units.

Miami burst pipe insurance claims often get underpaid. We document hidden water damage — moisture migration, subfloor saturation, mold formation — and fight for the full settlement you deserve.

Industrial steel facility damage claims are complex. We evaluate structural losses and build expert-backed insurance claims for Florida businesses — corrosion, impact, fire, and storm-related steel damage.

Florida fire damage claims require thorough documentation. We help homeowners recover full insurance value for structural damage, smoke contamination, content loss, and code-required rebuild upgrades.

Florida waterfront estate insurance claims involve unique risks. We help coastal homeowners document hurricane, surge, and saltwater damage and maximize insurer recovery on high-value properties.

If the claim is small, well-documented, and the insurer's offer feels reasonable, you can often handle it yourself using the resources on this page. If the offer is well below the actual loss, if you've been denied, or if the insurer is stonewalling — that's where a public adjuster pays for themselves many times over. Most cases recover 3–5x more than the policyholder could negotiate alone. There's no charge for a review.

Most Florida policies allow you to reopen or supplement a claim for up to 5 years from the date of loss. Evidence degrades over time, so the sooner you act the stronger the file. Even if you've already cashed a check, you may still have rights to a supplemental claim. Contact us within the deadline and we'll tell you exactly where you stand.

We work on contingency. Our fee is a percentage of what we recover — not what you've already been offered. If we don't get you more money, you owe us nothing. The initial review is always free and there are no upfront costs at any stage of the process.

Yes — frequently. Closed doesn't mean final. If the original settlement undervalued the loss, missed damage, or excluded items your policy covers, we can reopen the claim with a supplemental scope. Hidden mold, foundation moisture, structural damage, and matching costs are commonly missed the first time.

A public adjuster handles the claims process — documentation, negotiation, appraisal. An attorney handles litigation. Most claims settle without litigation, which is why most policyholders start with a public adjuster. If your case requires legal action, we work alongside your attorney and our documentation supports the legal fight.

Whether you've just received a denial or been fighting an underpaid settlement for months — we can help. We respond within one hour. No obligation, no pressure — just a straight assessment of what your claim is worth.

No obligation · We respond within 1 hour