01

Hidden moisture, found

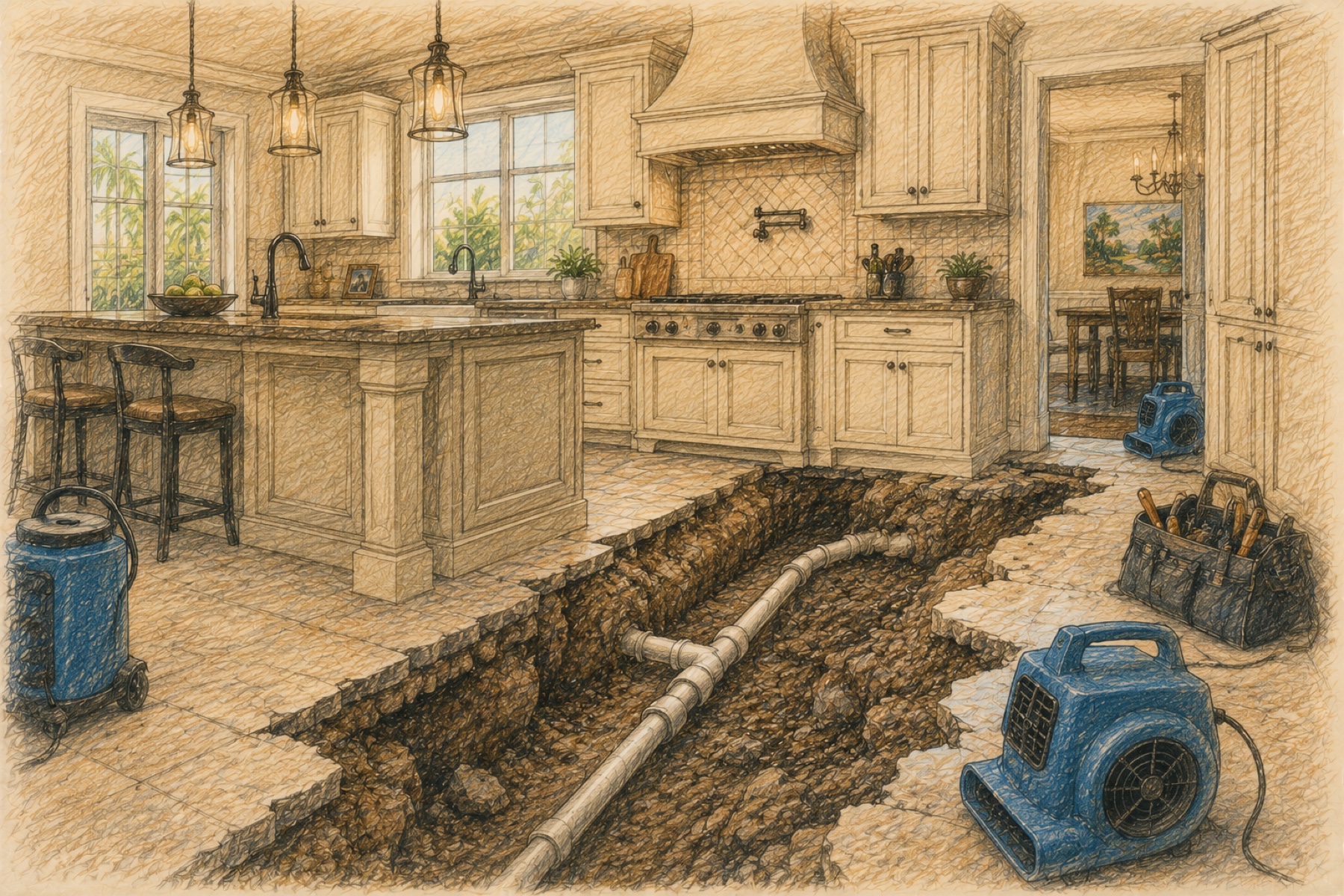

Insurance adjusters rarely use thermal imaging or moisture meters to map the full extent of water intrusion. We do — and the delta between what they find and what we find is usually measured in tens of thousands.

Insurance adjusters are trained to minimize water damage settlements. They measure what's visible and ignore what's behind your walls. Hidden moisture leads to mold, structural rot, and costs that compound fast — but only if your insurer accounts for them. We make sure they do.

Free Claim Review

No obligation. We respond within 1 hour during business hours.

Your insurance company dispatches an adjuster whose job is to protect the company's bottom line — not yours. They document what's visible: a stained ceiling, warped floorboards, a damp drywall patch.

What they don't measure — or choose not to — is the moisture migration spreading through your wall cavities, your subfloor, your structural framing. By the time the full scope of a plumbing-leak claim is understood, the gap between the first check and the real cost is already five to ten times wider. If your insurer already closed the claim, collecting that difference becomes your fight.

Insurance adjusters rarely use thermal imaging or moisture meters to map the full extent of water intrusion. We do — and the delta between what they find and what we find is usually measured in tens of thousands.

Mold caused by a covered water event is itself covered — but insurers routinely classify it separately, cap it at a low sublimit, or deny it as "pre-existing." We tie the mold directly to the original loss with scrutiny-proof documentation.

Insurer estimates exclude code-compliant repairs, matching finishes, temporary housing during remediation, and full content replacement. Our scope of loss captures every line item your policy already covers.

Claim Coverage

Every plumbing system failure and water intrusion source covered under your policy — we know how to document all of them.

Sudden pipe failures behind walls, under slabs, or in attic spaces. We document full moisture migration — not just the visible surface damage insurers prefer to acknowledge.

Condensate drain overflows, air handler pan failures, and duct condensation causing ceiling, wall, and flooring damage. Often misclassified as maintenance — we prove covered sudden loss.

Category 3 water intrusion from sewage backup or toilet overflow. Contaminated water events require full biohazard remediation — costs insurers routinely cap or deny without a proper fight.

Cracked liners, failed grout seams, and corroded drains let shower water seep into subfloors, joists, and the ceiling below. By the time the stain appears downstairs, framing is already rotting and mold has colonized the cavity — we document the full chain of damage and recover every dollar your policy covers.

Dishwasher, refrigerator ice maker, washing machine, and water heater failures. Sudden appliance water releases are covered — we document the damage scope before insurers minimize the claim.

Underground slab leaks causing floor buckling, foundation moisture, and mold. Among the most costly and commonly underpaid claims — requires specialized documentation we're experienced in building.

Water Damage Settlements

These are actual water damage claim outcomes. The insurer's initial offer is what they hoped you'd accept.

How It Works

We handle everything — so you can focus on restoring your home, not fighting your insurance company.

Step One

We visit your property, deploy FLIR thermal cameras and calibrated moisture meters, photograph all damage, and map the full extent of water migration — including what's hidden behind finished surfaces. This inspection is free and comes with no obligation.

Step Two

We prepare a comprehensive scope of loss including all damaged materials, restoration labor, mold remediation if applicable, code-compliant upgrades, matching finishes, and temporary housing costs. Every line item your policy covers is documented and itemized.

Step Three

We submit your claim, respond to every low-ball counter-offer, dispute misclassifications, and push back on exclusions that don't hold up to policy language analysis. We handle all correspondence with your insurance company so you don't have to.

Step Four

We don't close your file until you have the best possible settlement. If the insurer refuses to move, we escalate — invoking the appraisal clause if necessary. Our fee is a percentage of what we recover, which means our incentive is the same as yours: maximum recovery.

Insurance companies frequently misclassify covered water damage as "normal wear and tear" or "maintenance issues" to reduce or deny payouts. A licensed public adjuster can review your policy language, gather documentation of the actual cause of loss, and formally challenge that classification. Many "wear and tear" denials are overturned when properly disputed with supporting photographic evidence, moisture documentation, and a professional scope of loss.

Yes. You have the right to dispute an inadequate damage assessment. We use FLIR thermal infrared cameras and professional moisture meters to document hidden damage the insurer's adjuster missed. We then formally supplement the claim with this new evidence — and in many cases, this supplemental documentation recovers a settlement that's multiple times the original offer. The sooner you act, the better.

We use FLIR thermal infrared cameras to identify moisture trapped behind walls, ceilings, and under floors without destructive testing. We also deploy calibrated moisture meters to measure saturation levels, map the full moisture migration path, and document everything with detailed photographs and a written scope of loss. This documentation is what forces insurers to pay for the complete damage — not just the surface damage visible to the naked eye.

Absolutely. Mold resulting from a covered water loss is itself a covered claim in most homeowner policies. Insurers frequently deny mold remediation as a separate cost, claim it was "pre-existing," or apply a low sublimit without telling you about the full policy coverage available. We link the mold directly to the covered water event through documented evidence and timeline analysis, and fight for full remediation costs including structural repairs, air quality testing, and content replacement.

In most cases, yes — sudden and accidental water damage from an HVAC system is a covered peril under standard homeowner policies. The key word is "sudden." Insurers will try to argue the leak was slow and ongoing, which they classify as a maintenance issue and exclude from coverage. We document the timeline of the loss, the moisture migration pattern, and the specific policy language to prove the event qualifies as a sudden covered loss rather than a gradual leak.

Free Review

Whether you just had a burst pipe or you're fighting an underpaid settlement from months ago — we can help. We respond within one hour. No obligation, no pressure — just a straight assessment of what your water damage insurance claim is worth.

No obligation · We respond within 1 hour