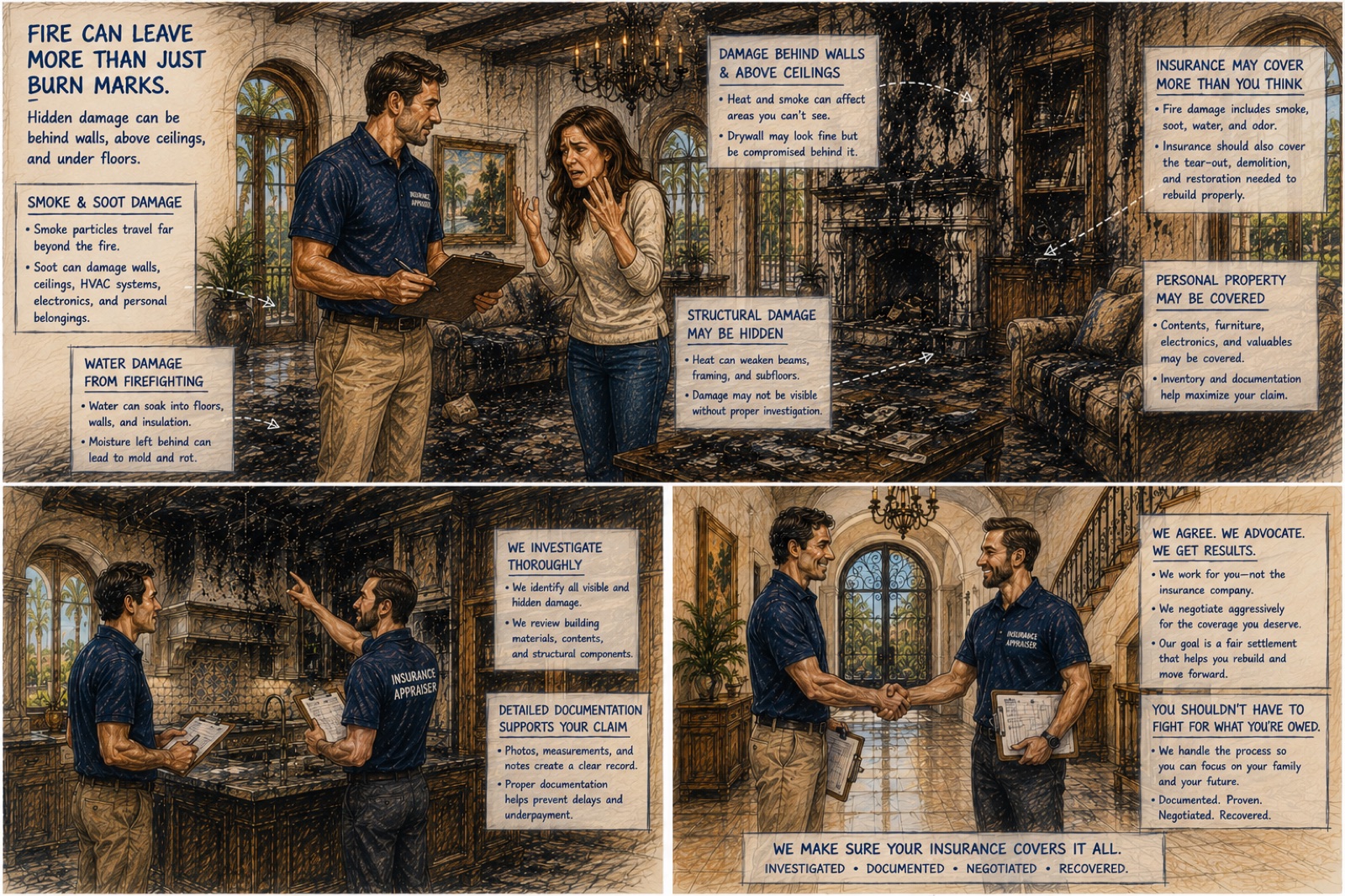

$138,000

Fire & Smoke — Residential

Palm Beach residential. Original scope missed whole-house smoke contamination, HVAC replacement, and contents. Appraisal award included full structural remediation and contents replacement.

Initial offer $39,000 → Appraisal award $138,000